With more frequency, communities are being asked to consider the option of installing a solar power facility. The decision to move forward with a solar power facility requires the evaluation of many factors. This article provides a brief overview of how the property tax vs payment-in-lieu-of-taxes (PILOT) options for a solar power installation project compare. The information is presented in a bullet point format for ease of use in discussions with your communities.

Property Taxes

Solar power installations are classified as Public Utility Tangible Personal Property (PUTPP). PUTPP valuation is set by the Ohio Department of Taxation (ODT) not by the county auditor (as is the case with residential, agricultural and business real property).

PUTPP equipment such as that involved in solar installations is broken into 3 categories:

Electricity production equipment (30-year depreciation);

Electricity transmission and distribution equipment (30-year depreciation); and

General business equipment (15-year depreciation).

The initial PUTPP valuation is generally based on the construction cost of the project and this value is then reduced for depreciation for up to 30 years.

Property that depreciates over 30 years has its value reduced by about 3.3% annually for 20 years and then by about 1.7% for 10 years.

Property that depreciates over 15 years has its value reduced by about 6.7% annually for 9 years and by a lesser amount for 6 years.

Ohio does not allow PUTPP property to depreciate below 15% of the initial valuation.

Depreciation means that solar property tax payments will decline over time until they level off after 30 years when depreciation hits the 15% minimum level (assuming a constant tax rate).

PUTPP taxpayers are allowed to appeal the valuation set by the ODT. The first appeal is to the state Tax Commissioner. If that is unsuccessful, the taxpayer can then appeal to the Board of Tax Appeals. If that is unsuccessful, the taxpayer can file a legal challenge which can go all the way to the Ohio Supreme Court.

Ohio’s recent history indicates that it is not uncommon for valuations of power generation facilities to be challenged after the property has been sold or when market circumstances change (for example coal-fired power plants). Thus, a change in the price of solar panels could conceivably impact the cost of a project and hence its taxable value.

If a facility is shut down its taxable value is typically reduced to $0. In this case both PUTPP tax payments and PILOT payments would be $0.

Ohio’s school funding formula functions so that if a school district gets poorer over time it will get more state aid and if school district gets wealthier over time it will get less state aid.

If the PILOT payment option is not taken, then the annual taxable public utility property value of the Solar installation within the district’s boundaries will be included in the school district’s wealth calculation. This will typically mean that the school district will get less state aid because it is now wealthier in the eyes of the state aid formula.

If a school district is on the transitional aid guarantee, then the increase in property valuation if no PILOT is granted will push it further onto the guarantee (meaning it will take the district longer to get back “on the formula”).

Payments-in-Lieu-of-Taxes (PILOTs)

Senate Bill (SB) 232 (2010) allows for renewable energy projects (such as solar projects) to be designated as “qualified energy projects” (QEPs).

If a project is designated as a QEP, then the project owner can make Payments in Lieu of Taxes (commonly referred to as “PILOT” payments) instead of paying property taxes based on the valuation of the project equipment’s PUTPP and the value of the land on which it sits.

SB 232 calls for an annual PILOT payment of $7,000 per MW to be split across all government taxing authorities where the project is located, with the option for an additional $2,000 per MW annual payment which would go entirely to the county where the project is located.

County Commissioners in the county where the project is located must vote to approve the PILOT payment by designating the project as a QEP.

Unlike PUTPP property taxes which will decline over time, PILOT payments are a constant amount every year for the life of the project so long as the “nameplate” generation capability (in MW) of the solar facility remains the same. As such, PILOT payment amounts are more certain over time than are property taxes because they are not subject to challenges by utility owners in the same way that PUTPP valuations (and hence taxes) can be.

Another critically important difference is that if the PILOT is granted the Solar property valuation is not included in the district’s wealth and its state aid is not reduced.

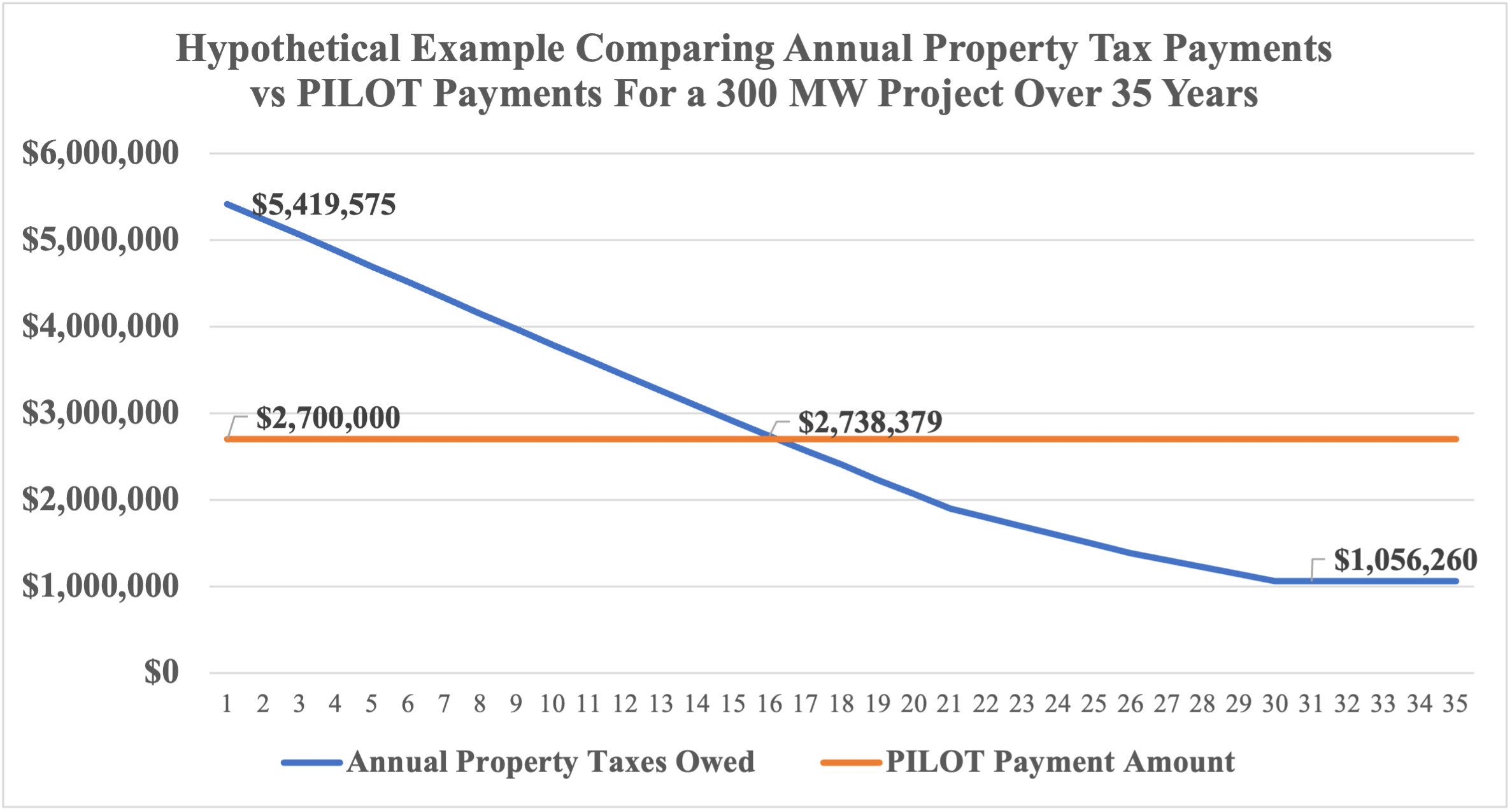

Property Taxes vs PILOT Payment Comparison Over Time

The graph shows year-by-year property taxes vs PILOT payments for a hypothetical example where the total value of taxes and PILOT payments over the 35-year time frame are approximately equal. In this example, property tax payments are higher for the first 16 years while PILOT payments are higher for the remaining 19 years of the hypothetical 35-year project timeframe.

Conclusions

Based on the discussion above, the following conclusions can be drawn:

Total PUTPP taxes can be higher or lower than total PILOT payments over the life of a Solar project depending on local tax rates.

PUTPP taxes start out at a high level in year one and then decline over time due to depreciation. Depreciation stops in year 30.

PILOT payments remain the same each year.

Because PUTPP taxes start out high and then decrease over time, PUTPP taxes will typically be higher than the annual PILOT amount for the first 15-18 years of a project’s life and lower than the annual PILOT amount for the remaining years.

Solar utility owners have the right to challenge the assessed value of a project’s PUTPP equipment set by the Ohio Department of Taxation. This can mean that property taxes owed can change over time from pre-project estimates.

PILOT amounts are set in statute and are not subject to the same type of challenges as are property tax values. In this regard, PILOT amounts are more stable and predictable over time than are PUTPP taxes.

PILOT payments do not impact the state foundation aid formula.

However, if a PILOT is not approved the assessed PUTPP value of the Solar installation will be included in a school district’s property valuation and the district will appear wealthier when state aid is computed. This will typically result in a district either experiencing a reduction in state aid and/or becoming subject to the guarantee.